Last week, the New York Times published the story “Square Feet: Americans Went All-In on Self-Storage. That Demand Is Suddenly Cooling.” The piece argues that many developers, spurred by the pandemic to invest money in new self-storage facilities, have been caught short by this drop in demand. While the story does contain many truths, like the Wall Street Journal self-storage story before it, it does not consider certain industry nuances – many of which could be found by picking up a copy of our 2024 Self-Storage Almanac (which is why we’re sending them a copy, on the house).

Occupancy

The NYT reports that occupancy has slowed – but slowed from what time period? Of course occupancy is down from the COVID era. During 2020-2022, self-storage saw unprecedented levels of occupancy. The NYT did recognize this, writing, “a wave of city dwellers fled their homes and offices closed, many searching for more outdoor space and residences closer to family. As people moved from apartments and condominiums, they often needed a place to put their stuff — and storage businesses raced to meet that demand.”

However, the outlet continues to drive home underperforming occupancy with this quote from Michael Elliott, an equity analyst at the investment research firm CFRA: “We’re probably closer to what would be a quote-unquote bottom with occupancy and rental rates,” he writes.

However, the outlet continues to drive home underperforming occupancy with this quote from Michael Elliott, an equity analyst at the investment research firm CFRA: “We’re probably closer to what would be a quote-unquote bottom with occupancy and rental rates,” he writes.

Bottom? Not even close. That would have been during the Great Recession of 2008-09, when occupancy dropped to the mid-70s before self-storage rebounded, as it always does.

Additionally, while occupancy is down from the highs of COVID, the NYT doesn’t note that it has simply rebalanced; it is now back to where it was pre-pandemic, as evidenced by Table 7.1.

The chart also shows that these most current figures are healthy, as most industry operators strive to keep occupancy between 90 percent and 95 percent. “Some try to maintain 100 percent occupancy,” notes the Almanac. “Though it might seem counterintuitive, you are losing money if you keep your facility completely full. This leaves you with two options: add new units or raise rental rates.”

Based on this perspective, the most recent data places self storage occupancy right in the sweet spot.

Rates & REITs

The NYT reports that rental rates are down, but this is to be expected with any slowdown in demand. However, it makes a big point of highlighting SpareFoot’s online platform which allows people to search for storage units. “The average monthly rent for a unit in the United States was $85.14 as of March, down from $108.58 two years earlier,” states the NYT.

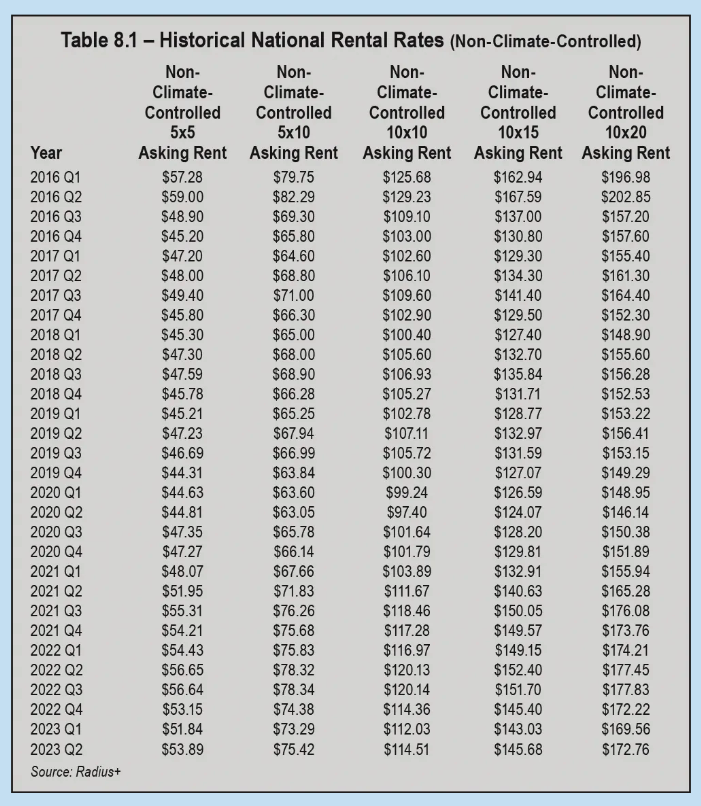

Again, this can be viewed as a bit of a course correction. Looking at national rental rates for climate-controlled units in Table 8.1, for example, we see that rates increased during the pandemic, as did demand. The post-pandemic cool off, naturally, would result in rates balancing out. However, they remain higher than pre-pandemic rates and even some of the rates during the pandemic.

More commentary on rates follows, with the outlet stating, “Storage companies have been making up for lower rates — usually offered as promotional prices — by raising rates on existing customers. The rate increases are happening at a much faster pace, too.” The NYT further quotes Kristin Millington, the director of self-storage and manufactured housing groups at investment firm Crow Holdings Capital, saying “Previously, the increases would happen after customers had been renting for around a year… Now, that’s hitting in month two or three — the move-in rates now are almost like a promotional rate.”

While some large operators have been implementing extreme rate hikes a few months after a tenant moves in – and MSM has addressed this in a series of articles and in the Almanac – it’s not necessarily because they’re performing poorly. Rather, they understand that most tenants tend to stay in a facility for 10 months or longer; so even if they miss out on some revenue in the first couple of months, they make up for it on the back end once the rate hikes have been implemented.

While we believe there should be more transparency about these rate increases with tenants, it’s also never been uncommon for REITs and other large operators to offer low entry pricing (Public Storage was famous for $1 move-in pricing for years). Additionally, REITs and large operators only represent a fraction of the self-storage industry.

“They’re not the majority,” says R. Christian Sonne, Executive Vice President & Specialty Practice Co-Leader–Self Storage at Newmark Valuation & Advisory. “There are plenty of independents that don’t play pricing games. They look for other ways to supplement income.”

Supply & Demand

The NYT reports that many developers who invested money in new self-storage facilities during the pandemic are now caught short by a recent drop in demand. It further cites a Yardi Matrix report that last year, 245 self-storage construction projects were abandoned, more than double the number from the year before.

While this is true, the story fails to acknowledge that the drop in demand is correcting a previous imbalance. “There was a staggering amount of new self-storage development across the country from 2016 to 2019 that diminished demand in some of the major metropolitan statistical areas (MSAs) and secondary markets within the United States into 2020,” reports the Self-Storage Almanac. It further states that post-COVID, supply chain issues, material shortages, and a lack of labor due to the pandemic caused new development to come to a temporary halt. “That brief hiatus, coupled with unprecedented pandemic-related demand for storage space and drawn-out approval processes for development, helped correct the imbalance,” concludes the Almanac.

That said, development is by no means dead. “Many professional, well-capitalized developers continue to find locations in major MSAs as well as secondary and tertiary markets for successful projects,” says Travis Morrow, Chairman/CEO of Store Local Corporation and the President of National Self Storage, though he adds that as with any development, a professional study should always be conducted before moving forward.

The NYT story seems to purport otherwise, however. “Higher interest rates make it harder for developers of storage facilities to finance construction,” the article concludes. This is in contrast to a new Self-Storage Association (SSA) report that was released Tuesday. In the report titled “Building Momentum,” the SSA states that “Despite the higher cost of construction and capital, new self storage supply is on the upswing and builders remain busy.”

The SSA also writes that contractors say business is brisk, and speaks with a number of industry experts from Baja Construction, Elevate Structures, MakoRabco, Morton Buildings, Steel & Metal Systems, and Trachte Building Systems. All six vendors are optimistic.

“Despite higher building costs in the industry, we are still seeing strong interest from clients wanting to build new self storage facilities and existing owners looking to expand their operations,” says Matt Milby, general manager of commercial business at Morton Buildings.

Kelly Crawford, executive director of operations at Steel & Metal Systems, concurs. “Construction in the storage market is thriving. Demand seems to remain constant and possibly growing.”

“Ultimately what we’re looking at is a reversion to mean, or a return to normal,” says Sonne. “Stock prices may be down, but the Times is forgetting that they were up 80% a few years ago. If you invested back then, you’re still doing great. Through boom and bust cycles, and even the great financial crisis, self storage performs better than any other real estate asset class.”

Challenges & Opportunities

When the big four REITs – CubeSmart, Extra Space Storage, National Storage Affiliates Trust, and Public Storage – released their financial statements for Q4 2023 in March, their CEOs were overwhelmingly positive, something the NYT didn’t report in favor of cherry-picking comments that mentioned any sort of challenges.

The NYT selected this quote from Public Storage’s president and chief executive, Joe Russell: “The new customer environment remains challenging.” However, it didn’t include this follow-up statement from the same call: “We are well positioned in 2024 with our operating model transformation enhancing the industry’s highest margins, our high growth non-same store pool comprising nearly 30% of the portfolio, and our balance sheet positioned to fund significant external growth.”

The outlet also uses this quote from Joe Margolis, chief executive of Extra Space Storage: “The industry as a whole will likely face headwinds from lower new customer rates in the near term.’” It fails to acknowledge, however, that immediately succeeding that statement, Margolis added, “We are confident in the durability of self-storage, our highly diversified portfolio and our platform's ability to capture customer volume when sector demand accelerates."

Further, the article leaves out Christopher Marr, president and CEO of CubeSmart, who said, “Looking to 2024, [CubeSmart is] well-positioned to execute our growth strategy in any macroeconomic climate,” as well as David Cramer, president and CEO of National Storage Affiliates Trust, who stated “[NSA] is in an attractive position to take advantage of external growth opportunities as they arise.”

The REITS have scheduled their Q1 2024 financial statement calls, which MSM will be sure to follow-up on.

Wrap Up

While the self-storage industry may never again see the unprecedented boom it experienced during the pandemic, the fact is the industry is resilient, and it continues to show its strength especially when compared to other real estate asset classes.

Angie Guerin, EVP with MakoRabco, even sees another benefit to the rebalancing. “I think a normalized market adds some runway for ideas to take root and innovation to thrive,” she told the SSA. “I think we’ll see some other great things developed by our industry in the near future.”

“Although trade area specifics can vary dynamically, I would say supply/demand overall is at equilibrium to under-supplied,” concludes Sonne. “Predictions for self-storage remain bullish, and our practice group appraised over 300 properties this past quarter. Things may be a little slower at the moment, but the powder is ready to be lit again.”

–

Brad Hadfield is the web manager and news writer for MSM.

Recent Posts

Senate Bill 709 (SB709) has many in the...

In January, self-storage industry veteran...

In April 1984, the first non-stop commercial...

Raise your hand if you’ve ever made plans,...

Everyone knows it: Investing in real estate...

They say when one door closes, another one...

Like its name implies, Surprise, Ariz., a...

Self-storage has become as reliant on the...

.gif)